Processing payment fees can be a big worry for small companies. But if you know what to look for, accepting card payments frequently pays off more than it costs.

Let’s start simple. What exactly is a payment processor? And what’s the difference between a payment processor and a payment gateway?

What is a POS Payment Processor?

A payment processor, or payment provider, authenticates transactions from the issuing bank (your customer’s bank) by verifying funds' availability or the credit card company's approval.

Payment Gateway vs. Payment Processor

Payment Gateway: A secured connection between your website’s shopping cart and the payment processor, necessary for eCommerce sites.

Payment Processor: Handles the transaction's processing, whether online or in-store.

So how does it all work?

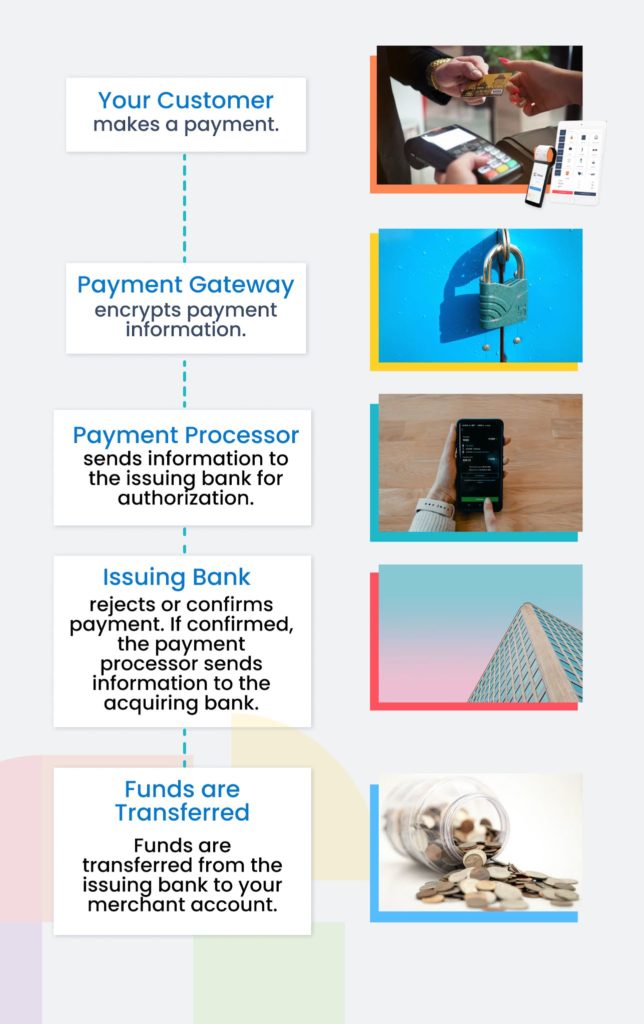

When your customer makes a payment online, the payment gateway encrypts your customer’s payment information to keep it secure. The information is then relayed to your payment processor.

If it’s an in-store payment, the payment information is directly relayed to your payment processor without the extra stop at the payment gateway.

The payment processor sends the information to the customer card’s issuing bank to check the authenticity of the payment details, and to determine if the customer has the funds to pay.

The issuing bank then responds to the request, either confirming that the payment can be made or rejecting the payment request.

If confirmed, the payment processor sends the information to your merchant bank account. The issuing bank transfers the funds to your merchant account.

Each of these steps comes with a small cost, which is where the processing fee comes from, and why payment processors take a percentage of your transactions.

How POS Payment Processing Works

Online Payments: The payment gateway encrypts customer payment information and relays it to the payment processor.

In-Store Payments: Payment information is sent directly to the payment processor.

Transaction Verification: The processor sends the information to the issuing bank to check the payment details' authenticity and fund availability.

Funds Transfer: If approved, the processor sends the information to your merchant bank account, and the issuing bank transfers the funds.

POS Processing fees

Processing fees are calculated per transaction – while the payment is being processed – so it’s hard to say exactly how much your processing fees will be, and what exactly your processor will charge you for.

Types of Processing Fees

Interchange fee: Every credit card company charges merchants a percentage-based interchange fee whenever a customer uses their card. This fee goes to the credit card’s bank and is intended to cover the cost of authenticating the payment.

This fee is based on a number and is charged by credit card companies to cover the cost of verifying the payment. The rate is affected by the type of card used, the amount being paid, the type of business, and the way of transaction (e.g., online vs. in-person). Most credit card companies, such as Visa and Mastercard, have their interchange fees published so you know the fee upfront.

Card brand fee: Also known as card association fees, these percentage-based fees go directly to the card company. They are typically less than the interchange fee.

Payment processor fee: Applied as a percentage-based or flat rate fee, this covers routing funds from the cardholder bank to the brand network and merchant bank.

Additional POS Fees

On top of these processing fees, you may also have other fees, including but not limited to:

Flat fees: Flat fees are typically negotiable and will vary depending on your payment processor. Some common fees include:

Annual fee: Yearly fee for using the payment processor’s service

Monthly fee: monthly fee for using the payment processor’s service

Batch fees: Charges for sending your daily batches to the bank

Network access fee: The credit card brand charges a fee for accessing their network

PCI fee: Some payment processor companies charge a fee to ensure that their merchants are compliant with PCI (Payment Card Industry Data Security Standard)

Statement fee: A charge for the preparation of your billing statement

Terminal fee: The cost of your payment terminal

Payment gateway fees: Whatever your payment gateway company charges for their services.

Situational fees:

As you might have figured out, situational fees are only charged when a specific situation arises. Here are a few common ones to watch out for:

Retrieval request fee: The fee when your customer requests a refund.

Chargeback fees: A fee when customers claim fraud or request a refund.

International fee: A fee when customers use an international credit card.

Monthly minimum fee: Charged when you don’t reach your minimum transaction total for the year.

Non-sufficient funds (NSF) fee: Charged when you don’t have the funds to pay your payment processor fees.

Set-up fee: The cost of setting up an account with a payment processor.

What else affects fees?

Keep in mind that other factors might affect your payment processing fees as well.

Type of card: Some credit card brands will have a higher processing fee than others. For example, American Express has a higher processing fee than Visa or Mastercard. Likewise, debit cards tend to have a lower processing fee than credit cards.

Payment method: The way your customer pays also has an impact on the payment processing cost. As a general rule, the less secure the method of payment, the higher the cost. For example, card-not-present transactions such as manually entering your customer’s credit card number have a higher cost because they’re less secure. On the other hand, mobile payments tend to be quite secure so they have a lower fee.

Business type: Larger businesses tend to have lower rates because they have a higher volume of transactions, and thus are more likely to negotiate for a better price. Smaller businesses don’t have the same power to negotiate lower rates since they have few transactions.

POS Pricing models

Interchange-plus pricing / Cost-plus

This is the most popular pricing model for a reason. It’s understandable, straightforward, and reasonable.

This pricing model consists of a small percentage of your transactions, a per-transaction flat fee, your card brand fee, plus your interchange fee.

Your payment processor fee, usually a percentage of your transactions plus a flat fee, and your interchange fee. The only downside is that its transparency can sometimes be overwhelming to some merchants, as every fee is spelled out in detail.

Flat-rate pricing

This pricing model offers a fixed percentage-based fee per dollar value of each transaction, typically with an added flat fee per transaction. This model is simple, predictable, and its monthly statements are easy to understand.

The downside? It’s easy to end up overpaying. While interchange fees vary, your flat rate is unwavering so you won’t get the opportunity to save costs, as you would with interchange-plus.

Tiered pricing

This pricing model is most beneficial for larger businesses that know how their customers pay. Tiered pricing typically segments your transactions into three categories – qualified, mid-qualified, and non-qualified (although this can differ by the payment processor). Every transaction is categorized based on your payment processor’s criteria – for example, different credit cards, or card-not-present transactions. Qualified transactions will come at a lower rate, whereas non-qualified transactions will come at a higher rate.

The downsides to this model are that the true costs are hidden. The pre-assigned rate for each tier hides the true cost of your transaction, so you very easily could end up paying more than you need to.

Integrated vs. Non-integrated payment terminals

Another thing to consider when searching for the right payment processor is whether you want a payment processor to integrate with your POS.

An integrated payment processor will connect with your POS to keep your payments streamlined on a single platform. This means whenever you’re ready to accept a payment, the information will automatically push to your payment processor. Likewise, once the payment has been made, it will push automatically to your POS.

A non-integrated payment terminal requires you and your staff to manually enter the payment into your payment terminal, and likewise manually complete the transaction in your POS after the payment has been processed. Non-integrated payment processors are more prone to human error – as you have to make sure you enter the right amount into the payment terminal and POS every single time, or else your numbers won’t add up at the end of the day. More and more businesses are opting for the convenience, efficiency and effectiveness of integrated payment solutions.

So what’s the right payment processor for you?

When selecting the ideal payment processor for your business, understanding your specific needs and comparing rates is essential. Our top recommendation is Oliver Pay. Oliver Pay offers enhanced security, 24/7 support, and competitive pricing tailored to different business types and countries, ensuring you get the best rates available.

Why Choose OliverPay?

Enhanced Security: We prioritize the safety of your transactions.

Around-the-Clock Support: Our team is available 24/7 to assist you.

Competitive Pricing: Our rates are customized based on your business type and location, ensuring you get the most cost-effective solution.